Dronehub licenses the autonomous-drone infrastructure. We don't sell drones to end users. That distinction is the load-bearing wall of the entire commercial model — and the most common point of confusion when buyers, journalists, or new partners encounter the company for the first time. This is the explanation.

The post unpacks why the IP-licensing model is the correct architecture for what Dronehub actually invents, where the three commercial doors sit, and what the structure means for the buyers, partners, and procurement evaluators who engage with us.

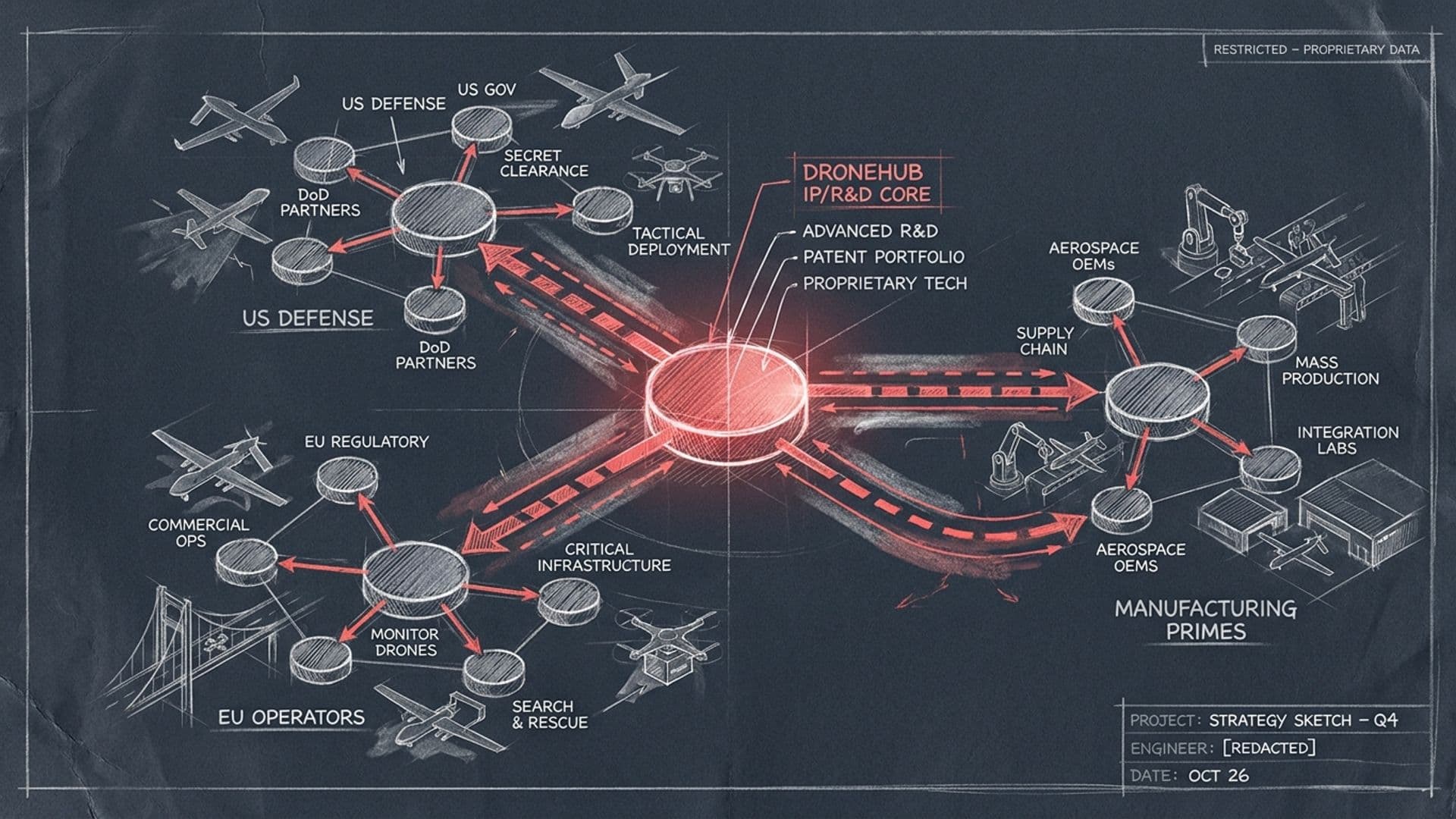

Three doors, not one

A drone company in 2026 typically operates on one of three axes. They sell drones to end users (the consumer / prosumer / commercial-direct model — DJI is the global archetype, with much of the Western market a category trail). They operate fleets directly (drone-as-a-service, where the company owns the assets and the operator runs missions for paying customers — Skydio's commercial arm, several inspection-services firms). Or they're pure software companies that layer analytics on top of someone else's hardware (a long tail of inspection-AI startups).

Dronehub sits on a fourth axis. We invent the IP, build the manufactured hardware in our own factory, and license the combined capability to partners who deploy it inside their markets. The three commercial doors are:

- IP licensing — for operators and integrators. The partner takes a deployment-ready capability (drone-in-a-box hardware, Sentinel AI stack, AUDROS counter-UAS, hybrid UAV-UGV) under licence, deploys it in their market under their brand and operational control, and pays a licence fee plus per-unit manufacturing.

- R&D partnerships — for governments and defense agencies. The funding agency co-funds a development programme (ESA, EDA, European Commission, Polish NCBR; increasingly SBIR/STTR in the US), Dronehub leads or participates in a multi-partner consortium, and the resulting IP becomes deployable across the broader licensee pool.

- Manufacturing — for defense primes and NATO-allied industrial partners who need non-Chinese supply chain for their own portfolios. The Jasionka factory builds units to the prime's specification under documented Section 848-compatible / EDIS-aligned terms.

Selling drones into the consumer or commercial-direct market is not one of the doors. It's not the door we forgot. It's the door we deliberately don't operate.

The fleet-ops trap

The most natural-sounding question — and the one that comes up first whenever a new partner encounters the model — is "why don't you just operate the drones yourself?" If the technology is good, why give it to someone else to run?

The answer is that operating drones and inventing drones are different businesses, and the companies that have tried to do both at scale have mostly done neither well.

Fleet operations require a different operational shape than R&D. The fleet operator needs local presence in every market they serve (a US drone-services firm cannot deploy in Germany without German operational staff, German regulatory licences, German customer relationships, and German liability cover). They need regulatory licensing per jurisdiction — every EU member state has its own UAV operations framework, the US has its own, the UK has its own, the Middle East has its own. They need 24/7 customer service per asset, because flight operations have weather windows and incident response and parts replacement. And they need continuous capital deployment that doesn't produce new IP — every dollar that goes into fleet expansion is a dollar that doesn't go into the next R&D programme.

The R&D investment that built Dronehub's portfolio — counter-UAS net-capture interception, AI rail inspection at Deutsche Bahn national scale, hybrid UAV-UGV with Galileo authentication, robotic battery swap, mobile docking — would have to compete inside the same company against the fleet-opex. The flywheel that converts EU public-programme funding into deployable IP would slow. The R&D bench that ships the next capability would be smaller. The advantages we built over six-plus years of consortium leadership would compress.

Most drone companies that tried to do both at scale found this out the hard way. The companies that scaled were the ones that picked an axis and stayed on it: the consumer-direct vendors (DJI), the pure operators (Skydio in commercial), the pure software plays. The middle ground burned cash without producing either operational excellence or durable IP.

Dronehub's model concentrates on the half that scales — the IP, the R&D, the manufactured platform — and lets partners do the half that's bounded by geography.

The IP licensing door

This is the largest customer category by buyer count. Operators and integrators who want a deployment-ready stack take Dronehub IP under licence and deploy it in their own markets.

Three properties of the licensing model matter to the partner. First, the IP arrives deployment-ready. The licensee isn't buying a research prototype — they're buying a stack that's been validated at production scale (Deutsche Bahn for AI rail inspection, AUDROS for counter-UAS, HUUVER for hybrid mobility, Nomad for mobile docking). Second, the manufactured hardware comes through Jasionka under documented sovereign supply chain — NDAA Section 848-compatible for US procurement, EDIS-aligned for EU defense procurement, traceable BOM for compliance-sensitive critical infrastructure. Third, the deployment support is structural: integration assistance, on-deployment model retraining (the AI taxonomy adapts to the licensee's specific asset class), and a back-channel for capability improvements that flow into the base architecture for all future licensees.

The buyers in this category are large enough to operate the technology themselves. Utility companies running grid inspection. Rail operators running track inspection. Port authorities running perimeter and asset-condition overwatch. Security integrators running critical-infrastructure counter-UAS. Prison-system contractors. Industrial primes deploying counter-UAS at refineries and substations. These are not consumers; they're enterprises with technical depth, procurement frameworks, and the operational scale to absorb a licensed capability.

Deal sizes range from low-six-figure per-capability licences to multi-million-euro multi-capability programme licences for major operators.

The R&D partnership door

This door is structured differently. Governments and defense agencies fund Dronehub-led or Dronehub-participating R&D programmes — ESA, EDA, European Commission Horizon, Polish NCBR, increasingly SBIR/STTR, AFWERX, and NATO DIANA on the US side. The agency funds the work; Dronehub leads or participates in the consortium; the resulting IP becomes deployable across the broader licensee pool.

The economics work on a different axis from the licensing door. The R&D programme funds the development cost directly (Horizon, ESA, EDA, NCBR grants typically cover 70-100% of the work depending on the instrument). The agency gets a national-capability outcome — a deployed technology that addresses a sovereign-capability gap. Dronehub gets the IP, the consortium-leadership credential, and the deployment-validation programme that becomes the reference for future commercial licensees.

This is the door that produced the AUDROS counter-UAS programme (ESA + EDA jointly funding an SME for the first time, European Defence Agency scoring Dronehub 98/100 on the CBRN counter-UAS evaluation). It's the door that produced HUUVER (Horizon 2020 #870236, first UAV with full Galileo OS-NMA authentication). It's the door that produced Nomad (Polish NCBR mobile-charging-station grant). And it's the door that produces the next generation of capabilities — the SBIR pipeline that runs through Dronehub Inc. and the EDF / NATO DIANA pipeline that runs through Dronehub Sp. z o.o.

R&D partnership is the engine that fuels the licensing door. Without the R&D depth, the licensing door has nothing to license.

The manufacturing door

The third door serves defense primes and NATO-allied industrial partners who need non-Chinese supply chain for their own portfolios. The Jasionka factory builds units to the prime's specification under documented Section 848-compatible / EDIS-aligned terms — sometimes under the prime's brand, sometimes as Dronehub-branded units that the prime integrates.

This is the smallest of the three doors by deal count but among the largest by deal value. Defense primes have specific platform requirements, demanding compliance documentation, and procurement cycles measured in years. The manufacturing engagements are structured as multi-year programme partnerships rather than per-unit purchases. The Jasionka line — which sits inside Aviation Valley, the densest aerospace and defense supply cluster in NATO Europe outside the major prime hubs — is the structural advantage that makes the door operate.

Manufacturing without IP doesn't work for Dronehub (we're not a contract manufacturer; the IP is the differentiator). IP without manufacturing also doesn't work for Section 848 / EDIS procurement (the buyer needs traceable provenance through the supply chain). The two propositions only work in combination, which is why the Jasionka factory exists in-house rather than as a subcontracted operation.

What this means for the partner

For US defense, federal innovation, and critical-infrastructure buyers — the door that fits depends on the buyer's role. Programme offices funding R&D engage through R&D partnership (SBIR/STTR, AFWERX Open Topics, DIU CSO, NATO Innovation Fund, NATO DIANA). Operational buyers procuring deployed capability engage through IP licensing (the AUDROS counter-UAS stack, the drone-in-a-box for critical infrastructure, the AI inspection capability for grid and rail). Primes building their own portfolios engage through manufacturing (Section 848-compatible hardware under their own designation).

For EU defense and industrial buyers — the same three doors operate, with EDF / NATO DIANA / national-MoD R&D on the partnership side, direct industrial licensing on the operator side, and EDIS-aligned manufacturing on the primes side.

For commercial critical-infrastructure operators — rail, energy, ports, refineries — the licensing door is the natural fit. Take the capability, deploy it in the operator's market under the operator's brand and operational control, with Dronehub providing the IP, the manufactured hardware through Jasionka, and the deployment-support layer.

The full IP licensing context lives on /ip-licensing. The R&D partnership doors — split between US and Europe — are at /rd-partnership/us-defense and /rd-partnership/europe. The manufacturing context is at /manufacturing. The full portfolio of projects deployed under the model is at /projects. The corporate structure context is at /about.

For a structured conversation about which door fits, open the contact form.

Key facts

Dronehub's commercial model has three doors: IP licensing for operators and integrators, R&D partnerships with governments and defense agencies, and manufacturing for primes that need non-CN supply chain. Selling drones to end users is explicitly not one of the doors.

Source · Dronehub commercial positioning

Dronehub has secured 6+ funded R&D programmes with the European Space Agency, the European Defence Agency, the European Commission Horizon programme, and the Polish National Centre for Research and Development (NCBR) — the portfolio is engineered around R&D depth, not fleet operations.

Source · Dronehub R&D programme record, 2018–2026

The Polish Jasionka factory ($7.5M production line, fully operational since 2025) builds for licensees, R&D partners, and manufacturing customers — not for Dronehub-operated fleets.

Source · Dronehub manufacturing operations record

The dual-domicile structure — Delaware C-Corp Dronehub Inc. (SBIR/STTR-eligible US small business) plus Polish Sp. z o.o. (Jasionka manufacturing) — exists to support the IP licensing and R&D partnership model, not to operate consumer or commercial drone fleets.

Source · Dronehub corporate structure

Vertical integration into fleet operations would require local presence per market, regulatory licensing per jurisdiction, and capital deployment that directly competes with the R&D investment that produces the IP in the first place — exactly the opposite of the durable advantage Dronehub is built on.

Source · Strategic analysis of vertical-vs-horizontal drone-industry models

The drone-in-a-box hardware, the counter-UAS interception stack, the hybrid UAV-UGV platform, the AI inspection pipeline, and the mobile docking system are all licensable IP blocks deployable by partners under licence — not standalone Dronehub-operated services in the consumer or commercial market.

Source · Dronehub product portfolio architecture

FAQ

- Why doesn't Dronehub just operate the drones itself?

- Because operating drones is a different business from inventing them. Fleet operations require local presence per market, regulatory licences per jurisdiction, customer service per asset, and continuous capital deployment that doesn't produce new IP. The R&D investment that built Dronehub's portfolio — counter-UAS interception, AI inspection at national scale, hybrid UAV-UGV platforms, sovereign supply chain — would have to compete inside the same company against fleet-opex. Most drone companies that tried to do both ended up doing neither well. Dronehub's model concentrates on the half that scales — the IP and the R&D — and lets partners do the half that's bounded by geography.

- Who actually licenses or partners with Dronehub?

- Three customer classes. First, operators and integrators who want a deployment-ready stack: utility companies running grid inspection, rail operators running track inspection, security integrators running critical-infrastructure overwatch, prison-system contractors running counter-UAS. Second, governments and defense agencies that fund R&D under sovereign-capability programmes: ESA, EDA, European Commission, NCBR, and increasingly SBIR/STTR through the US pipeline. Third, manufacturing customers — defense primes and NATO-allied industrial partners who need non-Chinese supply chain for their own portfolios. Each door is procurement-grade, with deal sizes that range from low-six-figure licence fees to multi-million-euro R&D programmes to multi-year manufacturing engagements.

- How is this different from a typical drone company?

- Most drone companies sit on one axis: they sell drones to end users (consumer, prosumer, commercial), they operate fleets directly (drone-as-a-service), or they're pure software companies layering analytics on top of someone else's hardware. Dronehub sits on a fourth axis — vertically integrated R&D plus horizontal licensing. We invent the IP, we build the manufactured hardware, and we license the combined capability to partners who deploy it in their markets. The closest analogues are defense IP houses (think specialist primes that license platforms to allied governments rather than operate them) and semiconductor IP companies (ARM is the canonical model — design the architecture, license to manufacturers).

- Does this mean Dronehub doesn't manufacture drones?

- We manufacture. The Jasionka factory in Aviation Valley, Poland — $7.5M production line, online since 2025 — builds the hardware for licensees, R&D partners, and manufacturing customers. What Dronehub doesn't do is sell those drones into the consumer or commercial-direct market. The factory output flows to partners who either deploy the drones in their own operations (operators/integrators) or rebrand under their own portfolio (manufacturing customers, primarily defense primes). The IP, the manufactured units, and the supply-chain provenance travel together; the fleet operations stay with the partner.

- What does an IP licensing deal look like in practice?

- Three structural elements. First, the IP scope — which capability blocks are licensed (e.g. drone-in-a-box hardware with the robotic battery-swap mechanism, Sentinel AI stack with a specific asset taxonomy, AUDROS counter-UAS interceptor with Eagle One platform). Second, the manufacturing path — Jasionka builds the units, the partner takes delivery under defined supply terms (NDAA Section 848-compatible documentation, EU defence-industrial-strategy alignment). Third, the deployment support — training, integration assistance, model retraining as the operator gathers data, model improvements flowing back into Dronehub's base architecture. Deal structures vary from per-unit licences to portfolio-wide capability licences to multi-year programme-based partnerships.

- Is this a defense-only model?

- No. Defense is the largest single customer category — US federal innovation (SBIR/STTR, AFWERX, DIU), EU defense industrial (EDF, NATO DIANA, national MoDs), defense primes needing non-CN supply chain. But commercial critical-infrastructure operators are a large category too: rail operators (Deutsche Bahn-class deployments), energy utilities, port authorities, refinery operators. The licensing model works in any market where the customer has scale, regulatory exposure, and the operational sophistication to run their own deployment — which is most of the buyer surface that actually pays for the technology.